The cheque is still considered an important instrument for transferring funds in the financial sector worldwide. It is because of its safety. However, we hardly know how the cheque clearing process works.

How the money flows from one account to another via cheque?

The technology used in clearing the cheque?

If you want to know the answers to these questions you are in the right place. Let’s get into the depth of the Cheque Clearing Process.

Contents

How Cheque Clearing Process Starts

The clearing process starts with the deposit of a cheque in a bank.The cheque is passed to the bank or branch where it is drawn.

The cheque is forwarded for the payment if the funds are available otherwise bank can bounce the cheque.

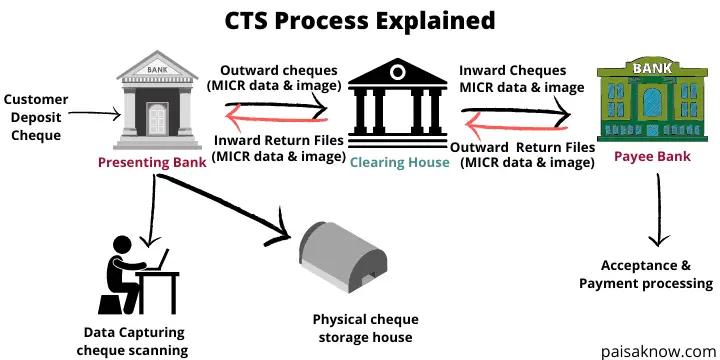

The cheque clearing process involves using the Cheque Truncation System(CTS) technology which helps the bank to speed up their work.

Let us understand about CTS in detail.

What is Cheque Truncation System(CTS)

Cheque Truncation system is a cheque clearing system introduced by the Reserve Bank of India(RBI) for faster clearing of cheque.

Truncation means stopping the movement of physical cheques from the presenting bank branch to the payee bank branch. Instead of a physical cheque, an electronic image of it is transmitted with important details like MICR Code, date of issuance, presenting bank, etc.

Read Also What is Canceled Cheque

Process Flow in Cheque Truncation System(CTS)

The transfer of the amount to any bank account through a cheque follows a few processes. below you can find them in detail.

- When you deposit the cheque to the bank officials they use CTS to scan it. In CTS the branch captures the important data from MICR band and images of the cheque using their capture system.

- To Ensure Safety and security of the information end to end public key infrastructure has been implemented in CTS.

- The Branch or the presenting bank sends the data and captured images duly signed digitally and encrypted to the central processing location (Clearing House) for onward transmission to the paying bank (destination or drawee bank).

- The paying bank and presenting bank uses an interface or gateway called the clearing house interface that enables them to connect and transmit data in a secure and safe manner to the clearing house(CH).

- The Clearing House processes the data, arrives at the settlement figure, and routes the images and requisite data to the paying banks.

- The paying banks through their Clearing House Interface (CHI) receive the images and data from the Clearing House for payment processing.

- The CHI of the paying bank also prepares the return file for the unpaid cheques, if any. The return files/data sent by the payment banks are processed by the clearing house in the return clearing session in the same way that presentation clearing and return data processing is provided to banks for processing.

- The clearing cycle is considered complete after the presentation clearing and associated return clearing session has been successfully processed. The entire essence of CTS technology for payment processing lies in the use of check images (rather than physical checks)

Read Also What is IFSC Code

Advantage of using CTS in Cheque Clearing Process

There are so many advantage of using CTS by the banks. some of them are listed below.

- CTS made clearing process shorter and faster through its technology.

- CTS stopped the movement of physical cheques hence it has eliminated the cost of moving physical cheques and saved time as well.

- It speeds up the process of collection of cheques therefore resulting in better service to customers.

- Reduction in operational risk and risk associated with paper clearing.

- Better verification and reconciliation process

New Approach to CTS Implementation

As we all know the technology keeps changing thus we need to upgrade our system to the latest technology. considering this RBI introduced a grid-based approach for cheque clearance.

As Per this approach the 66 MICR cheque processing locations consolidated in to three grids in New Delhi, Chennai and Mumbai.

Each grid provides cheque clearing services to all the banks coming under any particular grid.

Banks/branches/customers located in small towns or villages can deposit their cheques even if there is no cheque clearing system available.

The details of three grids are mentioned below.

New Delhi Grid: National Captial Region of New Delhi, Haryana, Punjab, Uttar Pradesh, Uttarakhand, Bihar, Jharkhand, Rajasthan, and the Union Territory of Chandigarh.

Mumbai Grid: Maharashtra, Goa, Gujarat, Madhya Pradesh, and Chattisgarh.

Chennai Grid: Andhra Pradesh, Telangana, Karnataka, Kerala, Tamilnadu, Odisha, West Bengal, Assam, and the Union Territory of Puducherry.

Read Also How to Transfer Money in PNB

Benefits of Grid based CTS Over Speed Clearing

The Grid-based CTS has an advantage as it covers a larger geographical area and there are very less chances that the paying bank will not present in the respective grid.

Under a grid-based cheque truncation system, all cheques drawn on the bank branches falling within the grid are considered as local cheques.

Cheque collection charges including speed clearing charges should not be levied if banks and payment banks are located under the jurisdiction of the same CTS grid, even if they are located in different cities.

Conclusion

Now we have learned how our deposited cheques get cleared by the banks. There are few process bank has to follow in order to process our cheques.

FAQs

1: If a customer desires to see the physical cheque issued by him for any reason, what are the options available?

Under CTS the physical cheques are maintained at the presenting bank and don’t move to the paying banks. just in case a client needs them, banks will offer pictures of cheques punctually certified/authenticated.

In case, however, a client needs to visualize/get the physical cheque, it’d got to be sourced from the presenting bank, that an invitation has got to be created to his/her bank.

To fulfill legal necessities, the presenting banks that truncate the cheques got to preserve the physical instruments for an amount of ten years. charges may add up in this process.

2: What are the precautions required to be taken by the customers to avoid fraud?

- Customers should use “CTS 2010” cheques which do not only image friendly but also have more security features. you can ask the bank to issue this cheque.

- Cheques not complying with CTS-2010 standards will not be cleared through CTS clearing.

- Avoid making alterations/corrections in the cheque. you can use a new cheque leaf in case if the previous one is altered/corrected.

Source: RBI