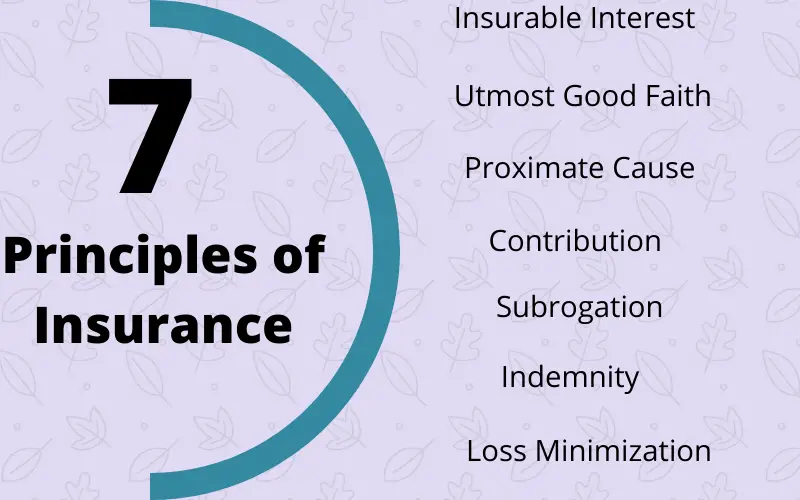

The concept of insurance starts by distributing the risks between people. Therefore in any insurance contract, cooperation becomes the basic principle of insurance. In order to ensure the correct functioning of the contract, the insurer and insured have to follow the 7 basic Principles of Insurance.

Lets Discuss these Basic Principles of Insurance one by one in detail.

Contents

Insurable Interest

The word interest has a different meaning in different scenarios. But here it means ‘financial relationship to someone or something”.

Insurable Interest is a person legal relationship to the subject matter of insurance that give them right to effect insurance on that.

In simple terms, We can say that if the insured person is having any insurance then he or she is legally eligible for any financial gain in case something happens like damage, destruction or loss, etc.For Example

Suppose a man had a whole life policy, who died some years later. When his wife presented a claim to the insurer, the latter discovered that at the time of the man’s death, they were no longer in the relationship of husband and wife. That means his wife had no insurable interest in the life of the deceased at the time of death.

Utmost Good Faith

This is the very primary and basic principle of all insurances. It means that the person who is getting insured has to disclose his complete and true information to the insurer.

In other terms, we can say that each party is under a duty to reveal all the key information to the other party, whether or not the other party asks for it.

Examples – the proposer of fire insurance is required to reveal all the loss that happened to the insurer even though it is not mentioned/asked in any form/insurer.

In the case of health insurance, a person should disclose the existing disease to the insurer before buying, and also the insurer should tell clearly what are the things that cover/not cover under any policy in detail.

In any case, if any parties (insurer and insured) try to hide the information there will be a breach of the Utmost good faith principle. Disclosing the things from both ends can develop good understanding and faith between them.

Proximate Cause

This is also called ‘Causa Proxima’ or the Nearest Cause. This is applicable when the loss is a result of two or more causes.

Why is it important to find out which of the causes involved in an accident is the proximate cause?

It is because a loss might be the combined effect of a number of causes. The insurance companies will find the nearest cause of the loss of the property.

If something is insured in the proximate cause then the company has to pay compensation. If it is not a cause that something is insured against, then no payment will be made by the insurer.

Let us try to understand through an Example:

Ramesh has insured by a personal Accidental policy. one fine evening he took his car for a long drive and while driving he felt pain in his chest and because of a heart attack he collides his car with another car and Ramesh dies on the spot.

When his family claimed against his death with the insurer, the company investigated and found that the death happened not because of an accident but because of a heart attack. Therefore insurance company is not liable to pay anything since the proximate cause is a heart attack, not an accident.

Contribution

This Policy applies in the event of a double insurance policy for the same subject matter.it states the same as the principle of indemnity i.e. the insured can not make a profit by claiming one subject matter from different policies or companies.

This principle insures mostly equitable distribution of losses between different insurers.

For Example –

Suppose husband and wife insure their home and their contents from two different insurance companies each one thinking that others would forget to do it. If there is a fire and the INR 5,00,000 is the damage,

they will not receive INR 10,00,000 Compensation. Both the insurer will share INR 5,00,000 loss.

Calculation of Contribution

Contribution= Sum assured with individual Insurer/Total Sum assured*Total loss

A insured his home against fire with 2 insurance companies X and Y with Rs 30000 and Rs 40000. A fire took place at his home and there is a total loss of Rs 60000 was calculated.

Contribution of company X = 30000*60000/60000=30000 similarly

Contribution of company Y =30000*60000/60000=30000

So both companies X and Y will contribute Rs 30000 each.

“Above insurance Principle is applicable in all type of insurance contracts except Life insurance”

Subrogation

It means one party stands for the other. In simple terms, Subrogation is the transfer of rights and remedies of the insured to the insurer who has compensated the insured in respect of the loss.

Subrogation allows insurers to pursue claim proceedings against the third party to the extent of their insurance payments. In common law, an insurer should be subjected to action in the name of the insured.

Example –

Suppose a car, covered by a motor insurance policy is damaged by the negligence of a building contractor. The motor insurer will have to pay for the insured damage to the car.

As against the negligent contractor, The insured’s right to recover will not be affected by the insurance claim payment. However, the motor insurer may after compensating the insured take over such right from the insured and Sue the contractor for damage in name of the insured.

Some other consideration

In the law, subrogation rights are only acquired after compensation has been provided to the insured.

The insurer cannot recover more under subrogation than he has paid as compensation. for an instance-suppose, there is a loss of an antique by the insured. The insurance company pays for the claimed amount, and sometime later when the antique is found, its value is much higher. The insurer can only keep an amount equal to what he has paid and any balance belongs to the insured.

In case of subrogation emerging after abandonment of the property to the insurer, all the rights in the property belongs to the insurer.

Indemnity

Indemnity means an exact financial compensation to the insured i.e no more no less. This principle states that insurance is not to make a profit but only to compensate for the losses that occurred. Therefore the insured should not have any benefit from the insurance contract.

This principle is to restore the insured from the losses to the position he or she was in before.

In other words, the insured should be compensated for an amount equal to the actual loss and not an amount greater than the loss.

The indemnity principle is intended to set the insured back in the same financial position as it was before the loss occurred.

For Example–

Suppose a person has a car and it is insured for INR 5 lakhs.he met an accident and his car is damaged. The cost of the damage is 1 lakh and he claimed the loss of 5 lakhs to his insurer. In this case, he will not get the full amount but only 1 lakh he will receive.

Loss Minimization

This insurance says that being an owner of anything you have to be careful and take necessary steps to minimize the loss of the insured property in an uncertain event.

The principle does not allow the owner to be irresponsible or negligent just because the subject matter is insured.

For Example-

Suppose there is a small fire at the home. In case if the home and its contents are insured through Home Insurance the insured person can just sit ideal and relax thinking his home and its contents are secured, he will get the claim for sure.

If it is in his control he should try to control the fire like calling the fire department, throwing water, using a fire extinguisher if available, etc. if he does not do it it’s a violation of this principle.

Conclusion

The above Basic Principles of Insurance will help you to understand the insurance in detail. just because you have insurance does not mean that your claim will approve/paid every time. the insurance companies work on the above-mentioned Basic principles and every claim adjusted or approved keeping the same principles in mind.

Each one of the above Principles on Insurance has a relationship with each other and can not be separated from each other.